As the college football industry is remade, municipal bonds are part of Florida State University’s plans to generate more revenue from its program.

The Florida State University Athletics Association plans to sell $327 million in football-related bonds as soon as next week in a deal managed through the state’s Division of Bond Finance.

The Series 2024A and 2024B bonds are rated Aa3 by Moody’s Ratings and AA-minus by Fitch Ratings. The outlooks are stable.

Adobe Stock

Proceeds from the bond sales will be used to make substantial renovations and expansions to the FSU football stadium in Tallahassee and to build a football operations building.

The Series 2024A, with a par of $291.6 million, will be tax-exempt and have serial maturities from October 2024 to October 2053. The Series 2024B, with a par of $35 million, will be taxable and have serial maturities from October 2024 to October 2028.

The Series 2024A bonds will be subject to an optional par call from October 2034 onwards.

The bonds will be sold as early as next week, said a professional at the Florida Division of Bond Finance, who declined to be identified. “The division will monitor market conditions to determine the actual sale date and will provide notice through TM3 at least 18 hours prior to sale,” the professional said.

The bonds will be sold competitively.

“Per the state’s debt management policy, we sell all debt through competitive sale unless there are legitimate business reasons for a negotiated sale,” said the division professional. “Given the strength of the credit, including significant pledged revenues and AA-/Aa3 underlying ratings on the bonds, it was determined that a competitive sale for the bonds was appropriate.”

The bonds are being sold through the State of Florida Board of Governors and the state’s Division of Bond Finance is the issuer contact.

“We expect strong demand from investors for this inaugural issuance,” the division professional said. “The FSUAA bonds are backed by significant pledged revenues and the credit benefits from its strong alignment with, and strategic value to, Florida State University.”

In explaining Moody’s Aa3 rating, Vice President and Senior Credit Officer Dennis Gephardt pointed to the university’s Aa1 issuer rating, close strategic alignment with athletics, and prospects for active management of the finances.

The analyst said the

Gephardt also noted the university’s donor support, wealth of $2.5 billion, low debt burden, “strong operating performance,” and “well diversified” revenues including gains in sponsored research.

The Florida State University Athletics Association was restructured in 2019 to oversee the university’s Athletics Department and the Seminole Boosters, a not-for-profit corporation that raises money for the school’s athletic programs, according to an online investor presentation for the deal.

The Athletics Association is an example of

Its debt is secured by a first lien pledge of major recurring revenue sources for the Athletics Department and Seminole Boosters, including money from athletic conference TV contracts, ticket sales, booster donations, sponsorships and advertising, the presentation said.

“A thorough tax analysis has been conducted and focused on compliance with federal tax code rules related to private use,” the Division of Bond Finance source said, adding that the taxable series is being sold to account for the minimal private business use that occurs within the stadium.

“The taxable bonds are structured with short maturities in order to get the more expensive taxable debt off the books as quickly as possible,” the division professional said, adding that The pledged revenues for FSUAA include capital gifts and donations for the 2024 project that are received within five years after issuance, and the taxable debt features an accelerated maturity schedule based on the projected pledged gifts and donation revenue.

Byant Miller Olive P.A of Tallahassee, Florida, is the bond counsel on the deal.

U.S. Bank N.A. is the bond registrar and paying agent.

A portion of the pledged revenues are committed to prior lien obligations of the FSU Financial Assistance Inc. revenue bonds.

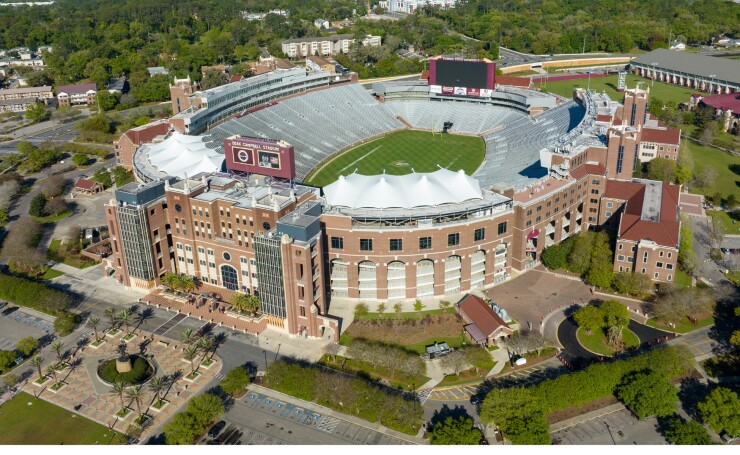

The bonds will fund renovations to seating at Doak Campbell Stadium, where 27,000 bleacher seats will be replaced by 16,500 more comfortable seats, suites and luxury boxes, with the goal, according to the offering documents, of raising more revenue from premium-price seating while lowering overall capacity to between 65,000 and 70,000 from 79,560. The university reports average attendance of 78,711 for last season’s six home games.

Proceeds also fund a new 150,000-square-foot operations facility for the football program, which will hand down its existing facilities to other varsity sports.

The gross pledged revenues of $93.3 million in fiscal year 2023 covers pro forma maximum annual debt service by 3.67 times, Gephardt said. “Our credit opinion considers the potential expense pressures of the athletic department as well as the potential volatility of intercollegiate athletics.”

The turmoil in the college sports industry is referenced in both the investor presentation and the preliminary official statement.

The context includes recognition of individual athletes’ rights to commercialize their names, images and likenesses, as well as conference realignments driven by college football TV and media contracts.

Realignment is “a phenomenon that has seen several prominent athletics programs voluntarily relinquish their traditional conference affiliation in favor of membership in a more financially lucrative conference,” the POS says.

Florida State is one of them. The program, which the offering document notes has won 16 Atlantic Coast Conference football championships since joining in 1992, is looking for an exit.

FSU, according to the offering document, “has publicly conveyed its dissatisfaction over an expanding revenue gap between the ACC and competing conferences, namely the SEC and the Big Ten.”

Because of that, according to the POS, FSU sued the ACC in December alleging mismanagement of the conference’s media rights, seeking the ability to leave the conference without paying a stipulated “exit fee.”

Rating analysts said they were aware of FSU’s litigation concerning exiting the Atlantic Coast Conference.

Withdrawing from the ACC could potentially cost the university $140 million plus the ACC’s lost broadcast revenues. The Fitch rating incorporates an “expectation that FSU will navigate through resolution while minimizing impact to its pledged revenue base and without jeopardizing any financial covenant performance,” the analysts said.

Fitch Director Nancy More, Director George Stimola, and Senior Director Emily Wadhwani said Fitch’s AA-minus rating of FSU Athletic Association’s incorporates FSU’s AA-plus issuer default rating, the “limited and relatively narrow pledge” of the FSUAA, and consideration of the “accompanying potential variability of athletics-related revenues and expenses.”

It also incorporates the “close and integral relationship” between FSU and FSUAA, the analysts said.

FSUAA had pledged revenue of $93.3 million in fiscal 2023. While far less than the university’s $1.76 billion, the association’s revenue “has proven resilient historically through economic stress despite the inherent risk of operating volatility,” they said.

In explaining revenue defensibility, they said in fiscal 2023 the association had contributed $141 million in athletic-related operating revenues.

Revenue defensibility is reinforced by the university’s status as a “comprehensive flagship research” institution with a broad draw for students. Student retention rates and average SAT scores are “very high.” Enrollment has remained steady in the last few years.

FSU operating revenue increased 11.3% in fiscal 2023 from fiscal 2022.

As for its operating risk rating, the university has a track record of “sufficient cash flow margins.” The analysts calculate the adjusted cash flow margin of 15.2% in fiscal 2023 and they expect fiscal 2024 will show a similar value.

FSU’s capital spending has been limited in “recent years but are ramping back up near-term, including the current project,” the Fitch analysts said.

As for their financial profile rating of the bonds, the analysts said they anticipated enough revenue to go above a 1.5 times coverage level. “An additional bonds test will require 1.5 times maximum annual debt service coverage based on average pledged revenues over the prior two fiscal years,” they said.