Municipals were little changed Wednesday as supply slowed and small inflows into muni mutual funds returned. U.S. Treasury yields fell and equities saw losses.

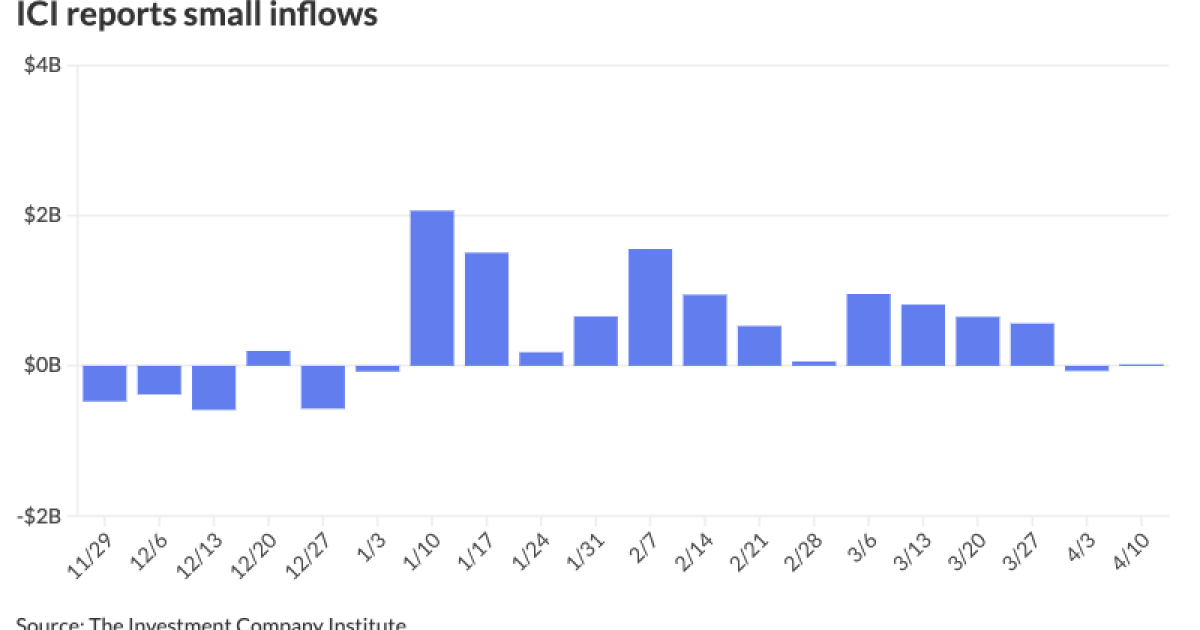

The Investment Company Institute reported small inflows to municipal bond mutual funds for the week ending April 10, with investors adding $18 million to funds following $69 million of outflows the week prior.

ICI reported exchange-traded funds saw inflows of $944 million following $19 million of outflows the week prior.

“The yield in all spots on the muni AAA HG curve hit new year-to-date highs, and the muni HG curve now shows outperformance across the curve this month relative to the broader fixed income market,” J.P. Morgan strategists said in a market commentary.

The “rapid” UST volatility is throwing munis “a bit of a curveball” regarding the magnitude of muni yield movements, said Jeff Timlin, a managing partner at Sage Advisory.

However, the volatility is

“You’d figure there’d be a little bit of softness there, people holding back, but there’s so much capital still out there and so much cash to invest,” Timlin said.

Another reason is that absolute yields “remain attractive in the context of the trading range over the past three years and our longer-term projections for lower rates this year,” J.P. Morgan strategists said.

Despite last week’s richening, the two-year investment-grade muni ratios compared to taxable fixed-income are at “transactional levels,” they said.

Ratios look “progressively richer” moving into the five- to 10-year part on the curve, with the 10-year spot “still far more attractive in taxables versus tax-exempts,” J.P. Morgan strategists said.

The two-year muni-to-Treasury ratio Wednesday was at 64%, the three-year at 63%, the five-year at 60%, the 10-year at 60% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 63%, the three-year at 62%, the five-year at 59%, the 10-year at 60% and the 30-year at 81% at 3:30 p.m.

The longest part of the curve in the tax-exempt market has the most apparent value, with ratios of 30-year AA tax-exempts firmly in the middle of the trailing two-year range, they said.

“Based on a 21% tax rate, the taxable equivalent yield for 30yr AA 4% tax-exempts provides only a 4 bps spread pickup over similar structure corporates, the tightest level since March 2022,” J.P. Morgan strategists said. Thirty-year AA taxable munis “offer modest spread” versus similar structure U.S. corporates as well.

“Current valuations and expectations for technicals suggest underperformance in the less favorable technical environment in April,” they said.

April may be a softer period in general, due to the expected supply coming until the beginning of June, relative to the amount of money that needs to be reinvested through maturity coupon payments, Timlin said.

This softness, he said, offers a good entry point for investors looking to redeploy capital.

Bond Buyer 30-day visible supply sits at $8.93 billion. Reinvestment dollars will pick up beginning in June, running through August, typically the heaviest three-month period of maturity and coupon payments that need to be reinvested, Timlin said.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.38% and 3.15% in two years. The five-year was at 2.78%, the 10-year at 2.74% and the 30-year at 3.90% at 3 p.m.

The ICE AAA yield curve was little changed: 3.37% (unch) in 2025 and 3.17% (unch) in 2026. The five-year was at 2.78% (+1), the 10-year was at 2.78% (unch) and the 30-year was at 3.87% (unch) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 3.43% in 2025 and 3.20% in 2026. The five-year was at 2.80%, the 10-year was at 2.79% and the 30-year yield was at 3.89%, according to a 3 p.m. read.

Bloomberg BVAL was bumped up to a basis point: 3.40% (unch) in 2025 and 3.19% (-1) in 2026. The five-year at 2.71% (-1), the 10-year at 2.72% (-1) and the 30-year at 3.91% (unch) at 3:30 p.m.

Treasuries were firmer across the curve.

The two-year UST was yielding 4.935% (-3), the three-year was at 4.770% (-5), the five-year at 4.619% (-7), the 10-year at 4.588% (-7), the 20-year at 4.821% (-6) and the 30-year at 4.702% (-6) at 3:30 p.m.

Primary to come

The Arizona Board of Regents (Aa3/AA-//) is set to price Thursday $150.655 million of Arizona State University SPEED revenue bonds, Series 2024. Goldman Sachs.

The Washington State Housing Finance Commission (/BBB-//) is set to price Thursday $189.995 million of Radford Court and Nordheim Court Portfolio nonprofit revenue bonds, Series 2024, serials 2028-2039, terms 2044, 2049, 2054, 2059. Barclays.

The Oklahoma Capital Improvement Authority (/AA-/AA-/) is set to price Thursday $167.900 million of state facilities refunding revenue bonds, consisting of $121.360 million of Series 2024A, serials 2025-2030, and $46.540 million of Series 2024B, serials 2025-2034. RBC Capital Markets.

The Oregon Department of Administrative Services (Aa2/AAA//) is set to price Thursday 147.650 million of tax-exempt Oregon State Lottery revenue refunding bonds, consisting of $92.895 million of 2024 Series A, $29.465 million of 2024 Series and $25.290 million of 2024 Series D. Goldman Sachs.

Wake County, North Carolina, (Aa1/AA+/AA+/) is set to price Thursday $137 million of limited obligation bonds, Series 2024A, serials 2025-2043. Truist.

Competitive

Albuquerque, New Mexico, (/AAA//) is set to sell $111.850 million of GO general purpose bonds, Series 2024A, and GO storm sewer bonds, Series 2024B, at 11 a.m. Thursday.

Clark County School District, Nevada, (A1/AA//) is set to sell $200 million of limited tax GO building bonds, Series 2024A, at 11:30 a.m. Thursday.