Munis saw a weaker tone Wednesday as muni yields were cut up to five basis points, depending on the scale, marking a second day of selling pressure, as few deals priced in the primary. U.S. Treasuries were slightly firmer across most of the curve and equities were mixed.

“Much like other periods in recent years when the curve stalled and the ensuing path became upwardly yielding, the current cycle is following a similar trend,” said Kim Olsan, senior vice president of municipals at FHN Financial.

Munis “failed to show any directional bias” in mid-March, but then hit a small weak patch toward the end of the month adjusting higher by around five points, she said.

However, during the start of this month, the “impetus to track to a higher range isn’t only internally driven but has become prodded by USTs under additional pressure based on reduced expectations for rate cuts,” Olsan said.

“Most spots on the muni AAA HG curve are at or near year-to-date highs, and the muni HG curve showed significant underperformance across the curve in March, relative to the broader fixed income market, after sizable muni outperformance in February,” said J.P. Morgan strategists.

Absolute yields, they said, “remain attractive in the context of the trading range over the past three years and our longer-term projections for lower rates this year.”

Ratios, “the much-maligned metric,” are seeing some relief in recent months, Olsan said.

The two-year muni-to-Treasury ratio Wednesday was at 66%, the three-year at 64%, the five-year at 62%, the 10-year at 60% and the 30-year at 84%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 66%, the three-year at 65%, the five-year at 62%, the 10-year at 62% and the 30-year at 84% at 3:30 p.m.

“Generic benchmark yields tracked wider moves in USTs, adjusting higher by about 10 basis points ahead of key payroll data,” she said. “In the process, relative value has improved 3-5 percentage points to settle into the mid-60% area in the front end of the curve to reach high points of the last quarter.”

With last week’s underperformance, J.P. Morgan strategists said two-year investment grade muni ratios versus taxable fixed-income “have moved closer to the middle of the range over the past few years.”

Ratios appear to be “progressively richer” moving out from five to 10 years on the curve, with the 10-year spot “still far more attractive in taxables versus tax-exempts,” they said.

Barclays strategists expect muni ratios to stay rich, and possibly adjust slightly higher.

“Current valuations and expectations for technicals suggest underperformance in the less favorable technical environment in March and April,” J.P. Morgan strategists said.

In the primary market Wednesday, few deals were price. KeyBanc Capital Markets priced for the National Finance Authority (/BBB+//) $450 million of Wheeling Power Company Project taxable utility refunding revenue bonds, Series 2024A, with 6.89s of 4/2034 at par, callable 1/1/2034.

Investors still await several larger new-issues set to price Thursday, including the week’s largest new-issue from the California State Public Works Board (Aa3/A+/AA-/) with $918.295 million of Department of General Services May Lee State Office Complex tax-exempt and taxable lease revenue bonds as well as $500 million of taxable corporate CUSIPs from Cornell University.

The Bond Buyer 30-day visible supply sits at $11.61 billion.

For April, Barclays strategists think supply will be $30 billion to $35 billion, with net issuance ranging from $10 billion to $15 billion, not including $8 billion in coupon payments.

They expect redemptions to decrease in April and forecast around $20 billion in bond redemptions and about $8 billion in coupon payments

“A pick-up in issuance alone should not greatly affect the muni market; it would need to be coupled with rate volatility, and if that happens, tax-exempts should finally cheapen,” Barclays strategists said.

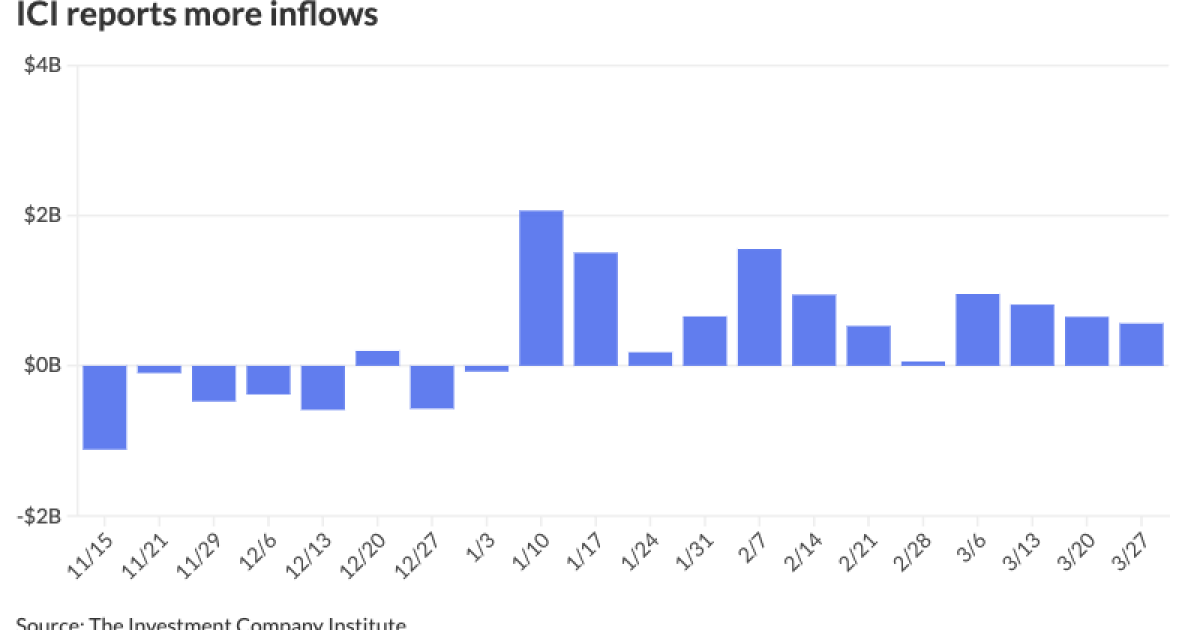

The Investment Company Institute reported more inflows into municipal bond mutual funds for the week ending March 27, with investors adding $564 million to funds following $652 million the week prior.

This marks 12 straight weeks of inflows.

ICI reported exchange-traded funds saw inflows of $740 million following $388 million of outflows the week prior.

AAA scales

Refinitiv MMD’s scale was cut up to two basis points: The one-year was at 3.34% (unch) and 3.11% (+2) in two years. The five-year was at 2.68% (+2), the 10-year at 2.63% (unch) and the 30-year at 3.78% (unch) at 3 p.m.

The ICE AAA yield curve was cut two to five basis points: 3.36% (+3) in 2025 and 3.12% (+5) in 2026. The five-year was at 2.72% (+4), the 10-year was at 2.67% (+2) and the 30-year was at 3.77% (+3) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was cut up to one basis point: The one-year was at 3.38% (+1) in 2025 and 3.12% (+1) in 2026. The five-year was at 2.69% (+1), the 10-year was at 2.65% (unch) and the 30-year yield was at 3.77% (unch), according to a 3 p.m. read.

Bloomberg BVAL was cut one to two basis points: 3.33% (+2) in 2025 and 3.10% (+2) in 2026. The five-year at 2.62% (+1), the 10-year at 2.61% (+1) and the 30-year at 3.79% (+1) at 3:30 p.m.

Treasuries were slightly firmer throughout most of the curve.

The two-year UST was yielding 4.675% (-3), the three-year was at 4.494% (-2), the five-year at 4.335% (-2), the 10-year at 4.352% (-1), the 20-year at 4.613% (flat) and the 30-year at 4.509% (+1) at 3:30 p.m.

Primary to come:

The California State Public Works Board (Aa3/A+/AA-/) is set to price Thursday $918.295 million of Department of General Services May Lee State Office Complex lease revenue bonds, consisting of $687.420 million of tax-exempts, 2024 Series A, serials 2034-2044, term 2049; and $230.875 million of taxables, 2024 Series B, serials 2025-2034. Barclays.

The New York City Housing Development Corp. (Aa2///) is set to price Thursday $323.335 million of sustainable development multi-family housing revenue bonds, consisting of $133.415 million of Series A-1 and $189.920 million of Series A-2. J.P. Morgan.

Chicago (/A+/A+/AA-/) is set to price Thursday $223.750 million of second lien wastewater transmission revenue refunding bonds, Series 2024A, serials 2025-2044. Loop Capital Markets.

The

The Pennsylvania Higher Education Assistance Agency is set to price Thursday $146.410 million of tax-exempt AMT fixed-rate education loan revenue bonds, consisting of $109.410 million of senior bonds, Series 2024-1A, and $37 million of subordinate bonds, Series 2024-1C. RBC Capital Markets.

The Shaker Heights City School District, Ohio, (/AA//) is set to price Thursday $102.660 million of unlimited tax GO school facilities improvement bonds, Series 2024, serials 2025-2044, terms 2049, 2054, 2057, 2061. Stifel, Nicolaus & Co.

Competitive